- Amanda Gillam

- 9th August, 2021

- Doorstep Loans

UPDATE 18 December 2021: Provident has confirmed that it is completely closing its doorstep lending business (Provident Personal Credit) on 31st December 2021. If you have any debt with Provident at this point it will be written off completely and you will not be required to repay it. If you have a continuous payment authority in place to repay your debt then Provident will cancel it automatically beforehand. If you make payments after this date then they will be repaid to you.

Provident Financial Plc is the largest subprime lender in the UK founded in Bradford in 1880. Over the last 140 years, the company has grown and tailored its core lending business to better serve the needs of its customers who were underserved by mainstream banks and credit companies. Of its three divisions, its Consumer Credit Division (CCD) that operates its home credit (Provident loans) and online (Satsuma Loans) is perhaps its most important. So, it is all the more surprising that Provident has been struggling with home collected loans in the last few years.

Provident’s Doorstep Lending Business

Provident’s doorstep loans business offers small value loans to people who are often excluded from mainstream credit solutions, whose incomes are often below the UK’s average and more likely than not to rent their home. Perhaps most importantly the customers do not have the luxury of savings to buffer them. Hence the access to small loans that they can repay on a weekly basis has been important. The average loan size is around £300. At any point in time Provident is lending to around 300,000 customers.

As of December 2020, the UK home credit market was worth £592m and Provident controlled 39% of that. Over the same period, the high-cost short-term market was valued at £184m and Satsuma HCSTC controlled 8% of this market. A portion of the UK market is met by local and regional providers. Provident is one of three national providers, the others being Morses Club and Loans at Home.

Provident Is Closing Its Consumer Credit Division

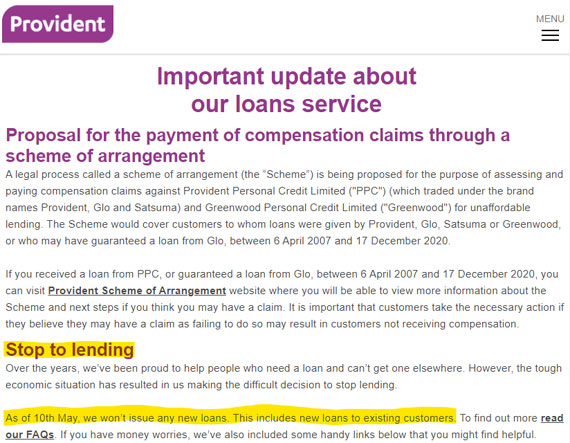

On 10 May 2021, the Provident announced it was stopping lending to both new and existing customers as it contemplated placing the division into a managed run-off or disposal. The only exception would be for customers who had already applied for loans and had signed the loan agreements. But why such a radical announcement? What’s gone wrong?

Some of the division’s weakness stems from mistakes it made in 2017. Back then it chose to move from a self-employed workforce of agents to a new employed workforce supported by new technology. Many of the agents chose to leave the industry rather than become employed. Others were picked off by their competitors. And the new support software created chaos for the collections process. The two problems combined such that the value of the business was significantly reduced. And the problems persisted over time.

On the back of this business weakness, Provident’s competitor Non-Standard Finance (NSF), owners of “Loans at Home”, attempted an unwelcome takeover of them in 2019. If nothing else this was a distraction that Provident could have done without. Provident managed to deter NSF but more damage was done.

Much more recently Provident has highlighted two other factors that have triggered its decision to exit the doorstep lending business:

Customer Complaints

Provident customers have increasingly been launching mis-selling complaints through Claims Management Companies. According to the claims, customers faulted the way Provident conducted its affordability and sustainability checks when handing out loans. The Financial Conduct Authority (FCA) jumped in to investigate the complaints specifically for loans issued between February 2020 to February 2021. In the first half of 2020, compensations for customer complaints cost PFG £25million a huge jump from £2.5million in the same period the previous year.

Financial Struggles

Even before Covid-19, the Consumer Credit Division had begun showing signs of financial struggle. When the pandemic hit, the operations worsened resulting in a £74.9m adjusted loss before tax loss for the division in 2020 compared to a £20.8m loss recorded in 2019.

What Happening Now?

To help address the impact of the rising consumer claims on its Consumer Credit Division, PFG on 15 March 2021 launched a Scheme of Arrangement, a legal method to help a company to restructure and aid it from financial distress.

Under the Scheme of Arrangement, Provident has sought to address claims arising from historic lending. These are claims relating to loans that were made between 6 April 2007 and 17 December 2020. Provident set aside £50m for the Scheme claims and a further £15m to offset the Scheme related costs, bringing the total commitment to £65m.

For the Scheme to be operational, it needed to be approved by the customers with redress claims and sanctioned by the High Court. The affected creditors are approximately 4.2 million.

The lender had warned that failure to have the Scheme approved, the Consumer Credit Division would have to be liquidated or put under administration. This would also mean that the customers with redress claims may end up not receiving any payment.

According to the Provident Financial Group board, the Scheme of Arrangement is the best bet and would ensure the interests of all parties – Consumer Credit Division, the Provident Financial Group, and stakeholders – are secured. Key dates have included:

- 22 April 2021 was the first court hearing where the Court ruled that CCD organise a meeting with the creditors of the Scheme to deliberate on the merits of the Scheme.

- 17 May 2021, the voting portal was opened to allow past and present CCD customers and the Financial Ombudsman Service to vote on the Scheme.

- 19 July 2021, the Scheme Meeting as provided for by the Court was held virtually and attended by over 428,000 creditors. Of these, 420,000 (98.1%) voted in favour of the Scheme.

- 30 July 2021, the High Court in its sanction hearing approved the Scheme of Arrangement by Order of 4 August 2021. This means that PFG will go ahead with the implementation of the Scheme and opening of the portal.

The FCA had its reservations about the use of a Scheme of Arrangement. They did not want consumers to suffer loss (i.e. get significantly less compensation than they are owed as per their redress claims), but when this was compared to the total insolvency of Provident Personal Credit Limited, the regulator decided not to move to court to block the Scheme of Arrangement.

What’s Next?

The Scheme became binding on 5 August 2021. Following the opening of the portal, customers will have until the end of February 2022 to submit their claims. If they fail to do so they will lose their right to compensation.

Provident expects that all compensation claims will have been assessed, settlements made, and the Scheme closed by the latter part of 2022.

Related Stories

Add a Comment

Categories

- Better Borrowing (215)

- Bad Credit Loans (23)

- Car Finance (28)

- Credit Brokers (11)

- Credit Cards (15)

- Doorstep Loans (13)

- Equity Release (3)

- Guarantor Loans (41)

- Logbook Loans (8)

- Mortgages (10)

- Personal Loans (16)

- Secured Loans (20)

- Short Term Cash Loans (31)

- Credit History & Credit Future (30)

- Ditching Debt (41)

- Household & Family (177)

- Better Budgeting & Saving (46)

- Cars – running costs (12)

- Energy bills (19)

- Food bills (13)

- Holidays (12)

- Mobile Phones & Broadband (11)

- Travel (11)

- Yourself (14)

- Income & Work (60)

- Money & Finance (168)

- News (90)

- Property (52)

- Home Rental (10)

- Home-ownership (43)

- Top Tips (106)

- Video & Infographics (30)

I was taken to court in 2018 and paid my debt of £2500 (settlement) to Provident – am i able to claim this back?

Dear Amanda gillam, my wife keeps getting letters from Lowell saying she owes 483.24 to provident. This was a doorstep loan over nine years ago, could you please tell Lowell that the debt has been written off and she does not have to pay it. You can contact them on http://www.lowell.co.uk or phone them on 03335565700. We have written to them on two occasions telling them this but they take no notice, please tell them to stop sending my wife letters. Many thanks Mr a ellis

Hello Mr Ellis. Unfortunately we are unable to help you as Provident was your wife’s lender, not us. I’m afraid you must persist with contacting Lowell if they bought Provident’s outstanding debts after they had gone into administration.

Provident Personal Credit with whom you had your loan no longer exists. The new legal entity is Vanquis Banking Group and we suggest you contact them.

Hi its Ann jones I’ve sent a cheque to me and provident and it was sold to a debt purchaser have you got the number for the debt purchaser as I can’t put my cheque in the bank as its got the wrong name on thanking you

Hello Ann. The best thing to do is call Provident using the contact details at https://www.providentpersonalcredit.com/contact-us/.

If they have gone out of buisness why are the agents still active seeking payments

About satsuma loans

Satsuma Loans, which is simply a brand name owned by the then Provident, has also ceased trading and its debts written off.

Provident hasn’t stopped trading. They’ve simply stopped making new loans. All existing borrowers are still required to make the repayments they originally committed to. Hence their team members will still visit to collect payments.

Suzanne, Provident has announced that they have indeed decided to close their doorstep lending business (Provident Personal Credit) completely on 31 December 2021. This means that any outstanding debt at that point will be written off by the business i.e. anyone in debt to Provident Personal Credit on 31/12/21 will no longer have to make any repayments. See our update to the blog post at the top.

I have received a letter this morning telling me not to make anymore payments??

Lynn, please see the update to our blog post regarding this. Amanda.

I have lost my letter from provident with my reference number. So I can apply to the compensation scheme where do I apply to get another reference number?

Hello Peter. If you visit https://scheme.providentpersonalcredit.com/ you’ll see that Provident have a helpline. Call them on 0800 056 8936 to resolve your issue. Good luck.