Car Leasing

- Long term car rental

- New & used cars

- Dealer & private sales

- All credit ratings

- Rates from 9.9% APR

- Rep. APR 19.9% APR

What is Car Leasing?

Car leases are long term car rental deals. You contract to use the car for a fixed period (say two to four years) but you are not looking necessarily to ever owning it. You pay a monthly fee that covers the depreciation of the car, the interest on the credit given to you and the road tax.

Car leases come in two flavours:

- Personal contract hire (PCH) – simple long term rental

- Personal contract purchase (PCP) – like PCH but with the option to buy the car at the end of the agreement

Our associate CarFinance 247 can find you great deals on your next lease contract. They’re the UK’s leading car lease broker and rated extremely highly by customers.

Car Lease Deals

- CarFinance 247 rated 4.6/5

- All credit ratings covered

- You get a dedicated adviser

- Car history check & valuation included

- No Fees!

- Questions about car leasing? Read our FAQs

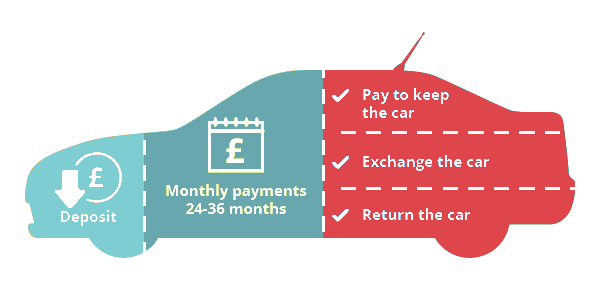

How Car Leasing Works

The basic principle of PCH and PCP car leases is the same:

- You make an up-front payment/initial deposit

- This is followed by fixed monthly payment for the duration of the contract (typically 2 to 4 years)

On the diagram below these are the blue areas. During the rental period you will have agreed to restrict your driving to, say, 10,000 miles per year. If you have exceeded this at end of the period then you will be expected to pay an excess of around 12p (estimate) per mile. As an example if at the end of the contract you have used the car 2000 miles more than you agreed you will pay an additional charge of 2000 x 12p = £240.

You will also need to take care of the car. If you hand it back with damage that is beyond simple wear and tear you will have to pay for it to be repaired (perhaps at a greater cost than if you had dealt with it yourself earlier). If your lease agreement is PCP then you will have two options over and above handing the vehicle back:

If your lease agreement is PCP then you will have two options over and above handing the vehicle back:

- make a final “balloon payment” and keep the car, or

- part exchange the car against a newer vehicle on a new PCP agreement

It’s this degree of flexibility that has made PCP so popular – it’s estimated that 80% of new cars are on a PCP contract.

There are some practicalities to be aware of:

- You can’t modify the car while you are renting it

- You obviously can’t sell the car unless you have bought it outright at the end of the contract

- You must comprehensively insure the vehicle

- You will responsible for paying for the service and maintenance of the car unless this is included in the rental agreement.

How to Choose the Right Car Leasing Deal

We’ve teamed up with CarFinance 247 who is one of the UK’s leading car finance brokers. We’ve chosen them because they offer excellent service (rating 4.6/5 on Trustpilot) and share our values. Their service extends beyond simply finding your car lease finance. They have an approved network of dealers you can use if you wish, and regardless of where you find your next vehicle, they will check its history and value for your peace of mind. And they do not charge any fee! If you are aged 17 to 21 then you could also consider Marmalade’s young person car finance.

1: Decide what you need

Consider both the amount you need to borrow and the amount you can afford to repay each month. Learn about car finance

3: Buy with confidence

CarFinance 247 can help you find a car to meet your needs if you haven't already got one in mind. They can provide a history check and valuation for peace of mind. Learn about CarFinance 247Aged 17-21? Learn about Marmalade

4: Get on the road

Once the lender has approved your application CarFinance 247 will pay the dealer for you and all you need to do is collect the car!

OTHER TYPES OF CAR FINANCE

Car finance covers a variety of financial products that enable you to buy a car. In addition to car leasing there are other options you may wish to consider. Click on the products you want more information about or compare them side by side.

Which type of car finance product may best suit your needs?

Car Finance Loans Guide

If you’re uncertain which type of credit might suit you or you have a money problem then one of guides may help you. We summarise each type of loan and their pros and cons, and address issues regarding debt and credit ratings.

Got a Question about Car Leasing?

Answers to Common Questions

Please note: this information is for guidance only. You should clarify the terms of the loan with the lender before entering into an agreement.

The answer to this question depends on what you are looking to achieve:

- use a new car at the minimum possible cost?

- own that new car you’ve always wanted?

- have a car that you don’t have to hand back after 2 to 4 years?

- drive as much as you like with no restrictions?

These forms of car finance are at opposite ends of the spectrum. In simple terms a hire purchase agreement is for those who want to eventually own the vehicle. Consequently, the monthly costs will be higher as you’re paying for the car in its entirety and not just covering its depreciation. A car lease is no more than a long term rental agreement at the end of which you hand the car back. You never own the vehicle.

There’s no right or wrong answer to this – it is a matter of personal choice. Find out more about your new car options.

Some of the factors to consider when making your choice will include:

- Is ownership something that bothers you?

- What’s the most you could afford to pay monthly?

- Do you have a deposit to put down?

- Can you readily control the mileage you drive?

- How frequently do you want to change your car?

- Do you want a new car or a used car?

The easiest way to get the best deal is to go through a finance broker who knows the car finance market inside out – so we suggest you use our partner CarFinance 247 who specialise in car finance. They will help you explore car lease and HP options as well as standard car loans.

You will then be better informed and in a better position to make a decision about the best way forward.

The answer differs for PCP and PCH forms of car leases:

For PCP – it is possible to get zero deposit contracts, but keep in mind that you will effectively be borrowing more and the monthly payment you will make will therefore be higher. If you are coming from an old PCP deal then it is possible that the vehicle’s actual market value is greater than its GFV (Guaranteed [Minimum] Future Value). If it is then this surplus can be treated as your deposit on a new deal.

For PCH – you will always have to pay an initial rental sum which will be at least 1 month’s fee. By paying more upfront you can reduce your monthly payments thereafter.

If you can show that you can afford the payments and have a reliable income then it is very possible you can get a car lease. This may even be the case if you are on a debt management plan or are on an IVA. You will need to be prepared to pay a higher rate of interest to cover the extra risk to the credit provider.

Credit agencies judge a car lease to be a significant financial commitment. As such entering into one will initially adversely affect your ability to get further credit – after all you’re in a contract where you’ll be making payments of £100s each month for a number of years.

So if you are thinking of getting a mortgage at the same time as getting a new car on a lease you may find it makes sense to arrange your mortgage first and then sort out a car lease after – you don’t want to enter a lease only to find that it stops you getting a mortgage.

Over time, as you demonstrate your ability to manage your finances and make your lease payments, you’ll actually see your credit rating improve.

Unlike PCP or HP car finance, car leases are not protected by section 99 of the Consumer Credit Act 1974. As such car leases do not have voluntary termination terms attached to them. So, ending a car lease/personal contract hire agreement early is likely to prove very expensive. You may have to pay off the remaining lease costs you have contracted to!

You cannot assume that it is possible to transfer your lease to another person. Some contracts don’t permit it. However, if it is allowed there are some things you will need to consider:

- You will probably have to find the person yourself

- The new party will need to be credit checked and approved

- There may need to be a minimum of 12 months left on the lease

- There is likely to be a significant administration fee charged

- A transfer will take a number of weeks to complete

Such a transfer is known as a Transfer of Contract.

Your lease agreement is a long term rental agreement. You do not have the option to buy the vehicle. You simply hand it back to the leasing company. But there are a number of things to be aware of:

- if you have exceeded your allowed mileage you will have to pay an excess charge calculated as the excess mileage multiplied by a rate per mile. You should check your contract for the specific terms

- if the car is damaged in excess of allowed wear and tear you will be charged for the repair

- if you want to extend the lease you may be able to, but this depends on the attitude of the leasing company

OUR REPUTATION

Our reputation is great. In fact we have scored 4.6 out of 5 based on 197 ratings & 30 user reviews for our car finance service.

THE SOLUTION TO YOUR MONEY PROBLEMS

Answer 4 quick questions and we’ll tell you what kinds of credit may be available to you

Use our quick, simple & secure enquiry form to get a quote now. Compare deals & complete your application.